While Ms. Cochran made several interesting points, one point that stood out was when she explained telling a founder seeking an investment to not quit his day job. While saying "I will not invest in your business" is a softer rejection, sometimes the tougher message is warranted if the founder is risking too much of his or her own time and money.

I have conveyed the tougher message when I feel the founder does not possess adequate skills to build a product or service of the highest quality, does not understand their customer or does not possess the knowledge or skills to build a profitable company (or more succinctly, the inability to build and lead a strong management team).

This does not mean that the founder should give up immediately. In a rejection to invest, I always hope the founder reflects on their method of communicating their proposal including their "path to success" as referenced in the previous post. Or the rejection will force the founder to reevaluate their plan to create a solution which will solve a problem people are willing to pay for on a scale that will generate sustainable revenue.

As with selling their product or service to a prospective customer, I also hope the founder will make another attempt to "close the deal" if the first attempt is rejected. When soliciting an investment from an investor, the founder should understand they are selling their business plan and investment proposal. In this blog post, I write about an article that contains a number of useful tips on raising capital including: "Absolutely follow up three times with an investor. No, you will not be scaring them away. Now, don't do it over a two-day span, but over a two to three week period. Follow up quickly and consistently."

A second point Ms. Cochran made that the audience seemed to appreciate was on the topic of when should a founder hire employees, She said she looks at the founder's schedule and if the founder is spending too much time on a particular activity that does not directly pertain to developing the product or generating sales, then it is time to hire an employee.

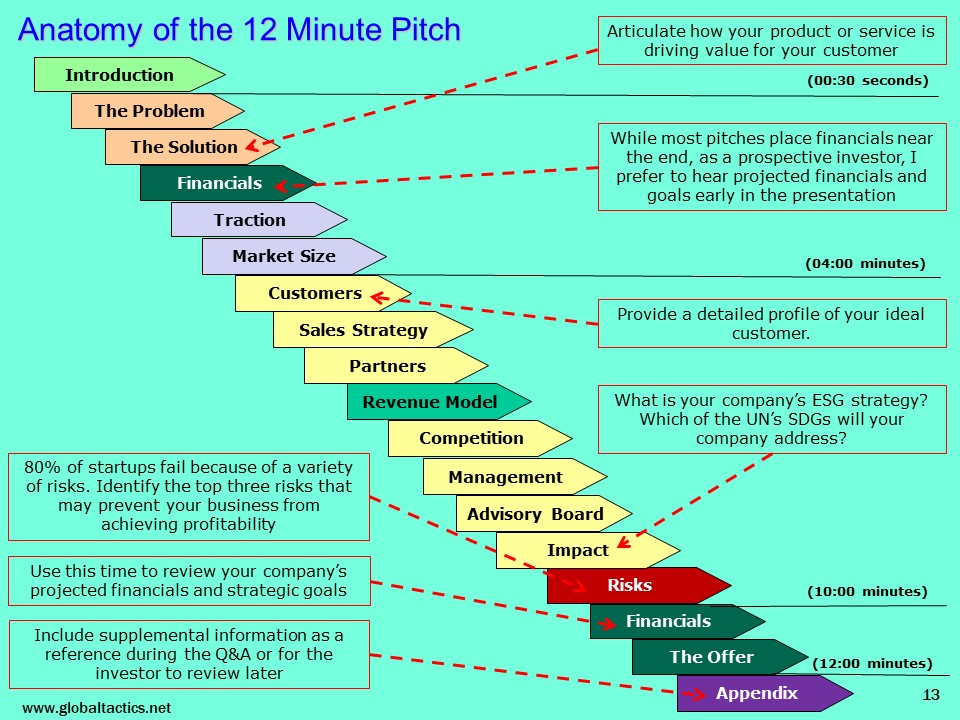

In addition to the discussion, a handout prepared by AoA listing ten tips for pitching angel investors was provided at the event:

Angel investors are entrusting you with their personal cash savings. Show that you are a steadfast individual who will be a good steward of their money.

2. Be transparent

It is better to accurately characterize the status of your company than to try to impress investors with grandiose claims. The moment you are less than forthright with facts, investors will walk away.

3. Simplify your message to express benefits, not features

Customers buy a product because it solves a need, not because of a rich feature set. Discuss the benefits of your product and the burning pain point it addresses.

4. Give investors the information they want

Don't start by trying to tell investors everything you can about your company. Focus on the highlights, and help them connect the dots on how you're going to build a game-changing business.

5. Act like your audience is trying to catch a bus

By getting to the point quickly and succinctly, you are demonstrating that you value investors' time, and that you will show similar respect to your team members, partners, and customers.

6. Use a bottom-up approach to determine market size

A top-down market analysis often relies on subjective, broad-brush assumptions and may not deliver a convincing estimate. The bottom-up approach substantiates your domain expertise and is often better anchored to customer demand and market realities.

7. Competition is a good thing

If there is no competition, chances are there is no market, and thus no business. Describing your competitive advantage and/or barriers to entry is an effective way to communicate how you will win in this market.

8. Be realistic

Your assumptions should be well thought out and attainable, though on the aggressive side. This is your opportunity to demonstrate nuanced business judgment and the scale of your ambition.

9. The numbers should add up correctly

Disconnects between market size, pricing, and financial projections are unlikely to impress investors. They may signal the lack of operational excellence and attention to detail that are crucial to building an iconic business.

10. In fundraising, all other startups are your competition

Most angel investors only have so many dollars to invest in startups, with lots of companies vying for that investment. If your proposed deal terms are significantly out of line with what other startups are offering, many investors will rather pass rather than risk antagonizing you by negotiating.

I strongly agree with the importance of building trust, which is done through being transparent. The moment I see gaps or inconsistencies in a founder's story is when trust is quickly eliminated.

"I love competition" is a saying I regularly convey to my colleagues. Competition conveys there is a market opportunity for our product and service. In addition, comparing ourselves to our competitors provides us with the opportunity to gauge our own performance.

Lastly, I wish founders were more realistic about the chances of building a profitable business. I am not saying they should be negative about their odds for success, but they should understand that most startups fail not for a lack of opportunity, but because of any number of risk factors or bad luck. And when a founder tells me the total addressable market is so big that all they need is to capture a market share of one percent in order to be successful, the words "no, I will not invest" quickly enters my mind.

Do you agree with Ms. Cochran's remarks? Do you have any tips for pitching angel investors?